Business & Money

Rural-Urban Credit Collapse: Catalyst of Kenya’s 1980s Financial Crisis

By 1984, the institution’s collapse marked the beginning of Kenya’s worst financial crisis, sending shockwaves through the banking sector and triggering the downfall of several local banks, including Union Bank, helmed by imminent stock broker Jimnah Mbaru, and Jimba Credit Corporation.

: The collapse of Rural Urban Credit Finance Ltd marks the start of Kenya’s devastating financial crisis in the 1980s and 1990s, reshaping the banking sector

By Charles Wachira

In the heart of Nairobi, Andrew Kimani Ngumba, a visionary former Mayor and MP for Mathare, spearheaded an ambitious financial initiative with the establishment of Rural Urban Credit Finance Ltd.

Named after him, Ngumba Estate, Nairobi, became synonymous with his commitment to uplift his constituents, primarily through the provision of unsecured loans for purchasing Volkswagen combis that operated on the Nyamakima-Mathare Number 10 route.

His intent was clear: to empower local entrepreneurs and enhance public transport.

However, this noble endeavor would soon unravel.

The rapid expansion of Rural Urban Credit Finance, fueled by a desire to meet soaring demand, resulted in reckless lending practices that laid the groundwork for disaster.

By 1984, the institution’s collapse marked the beginning of Kenya’s worst financial crisis, sending shockwaves through the banking sector and triggering the downfall of several local banks, including Union Bank, helmed by imminent stock broker Jimnah Mbaru, and Jimba Credit Corporation.

The fallout was swift and severe.

With mounting pressure from the government and furious depositors, Ngumba fled to Sweden in 1986, seeking refuge from the growing tide of public outrage.

Demonstrators vented their frustration by burning effigies of Ngumba, chanting slogans like “Ngumba: Mwizi!” (Ngumba: Thief!), a stark reflection of the deep-seated anger towards the financial collapse that devastated many lives.

In the wake of Ngumba’s exile, a by-election was held to fill the vacant seat, eventually won by Dr. Josephat Njuguna Karanja, who resigned as Vice Chancellor of the University of Nairobi to step into the political fray.

Meanwhile, from the sixth floor of Ngumba House,Nairobi Andrew Kimani Ngumba sought to rebuild his legacy by establishing three companies: Blue Shield Insurance Company, Kenyawide Building Society, and Countrywide Developers.

Buoyed by the performance of Rural Urban Credit Finance during its brief tenure, Ngumba launched Kenyawide Building Society to extend loans to individuals eager to develop their properties.

This new venture represented Ngumba’s attempt to restore his reputation and regain the trust of the public and the financial community.

Despite his efforts, the scars left by the collapse of Rural Urban Credit Finance were deep. The resulting economic turmoil of the 1980s and 1990s reverberated throughout Kenya, undermining confidence in the banking sector and leading to stricter regulations.

The ripple effect of Ngumba’s ambitious yet ultimately misguided expansion plans served as a cautionary tale of the perils of unregulated financial growth, shaping the landscape of Kenya’s banking sector for years to come.

As the dust settled, the crisis brought forth lessons on the importance of sound financial governance, regulatory oversight, and the dire consequences of unchecked ambition in the world of finance.

The legacy of Andrew Ngumba remains a complex narrative, intertwined with the rise and fall of a pivotal financial institution in Kenya’s history.

Keywords:Rural Urban Credit Finance Ltd:Kenya financial crisis:banking sector collapse:Andrew Ngumba:1980s economic turmoil

: Ethiopia attracts $53.5M in Q1 investments, creating 8,700 jobs. Growth driven

by reforms, with a focus on service and manufacturing sectors.

The Addis Ababa Investment Commission (AAIC) announced a promising start to the

2023/24 fiscal year, with 612 investors registering a combined capital of Birr 2.93 billion

($53.5 million) in the first quarter.

This reflects a 13% growth compared to the same period last year, signalling sustained

investor confidence despite economic challenges.

Speaking at a press briefing on November 30, AAIC’s Director of Communication,

Meseret Woldemariam, credited the growth to policy reforms and enhanced investor

facilitation.

“Our efforts to streamline investment processes and resolve bottlenecks are yielding

results. We remain committed to ensuring investors thrive in Addis Ababa,” she said.

SECTORIAL CONTRIBUTIONS

The majority of the newly licensed investors are in the service and manufacturing

sectors. The service sector includes hotels, tourism, and IT ventures, while the manufacturing

investments span electrical products, steel, wood, and textiles.

These investments have generated 8,707 jobs, comprising 770 permanent and 490

temporary positions created by newly licensed entities.

The AAIC has also initiated field monitoring visits to ensure operational readiness. “Our

team works closely with new investors to address challenges promptly, enabling faster

project rollout,” Meseret added.

CHALLENGES AND REFORMS

Investors continue to face hurdles such as foreign currency shortages and workspace

availability. However, the commission highlighted progress due to macroeconomic reforms,

particularly improving foreign currency access.

“We are actively collaborating with the Mayor’s office to address workspace issues

through professional support in rental solutions and operational guidance,” Meseret

explained.

Recent reforms in the National Bank of Ethiopia’s foreign exchange policy have also

been pivotal. In October, the central bank announced a 30% increase in forex allocation to priority sectors, a move welcomed by stakeholders.

EXPANSION PLANS AND PROJECTIONS

The AAIC aims to capitalise on the momentum, targeting Birr 15 billion ($274 million) in

investments by the end of the fiscal year. A new digital investment portal, launched in November, promises to reduce registration times by 40% and improve transparency.

“We are confident these initiatives will not only attract more investors but also deepen

the trust of existing ones,” Meseret concluded.

INVESTOR SENTIMENT

Prominent business leader Ahmed Yusuf, who recently launched a $3 million IT hub in

Addis Ababa, praised the commission’s efforts.

“The improvements in investor services and forex allocation are encouraging. We hope

to see more streamlined processes for licensing and operations,” he remarked.

As Ethiopia seeks to position itself as a regional investment hub, sustained efforts in

addressing investor concerns and enhancing infrastructure will be critical.

: Ethiopia’s December IMF review may unlock long-awaited debt restructuring,

crucial for economic reforms and stalled projects like the Koysha Hydroelectric

Dam.

Ethiopia’s much-anticipated debt restructuring prospects could gain clarity this

December, as the country awaits the second review under its four-year International

Monetary Fund (IMF) program.

The Extended Credit Facility (ECF), launched in August 2023, remains central to

Ethiopia’s economic reform and debt relief efforts.

Progress Toward Debt Treatment

Last week, Ethiopian authorities reached a staff-level agreement with the IMF tied to the

second review. A comprehensive report on this review is set for release in December, a month many stakeholders, including the National Bank of Ethiopia (NBE), view as pivotal for

advancing debt treatment plans.

“Debt restructuring stands at the centre of our reform agenda. With the report’s release,

we expect rescheduling talks to gain momentum,” said Habtamu Workneh, Director of

External Economic Analysis & International Relations at the NBE.

He added that discussions are focusing primarily on extending maturity dates for Ethiopia’s debts.

IMF Support and Engagements with Creditors

The IMF has provided Ethiopia with USD 2.5 billion under its current fiscal program,

offering critical support to the country’s macroeconomic stabilisation efforts.

In parallel, Ethiopian authorities have engaged with Eurobond holders and the Official

Creditors Committee (OCC).

A debt restructuring proposal was submitted to Eurobond holders in July 2024, following

key discussions in December 2023 and May 2024.

Additionally, a global investor update held on October 1, 2024, highlighted the nation’s

ongoing economic challenges and progress in creditor negotiations.

Shifting Debt Landscape

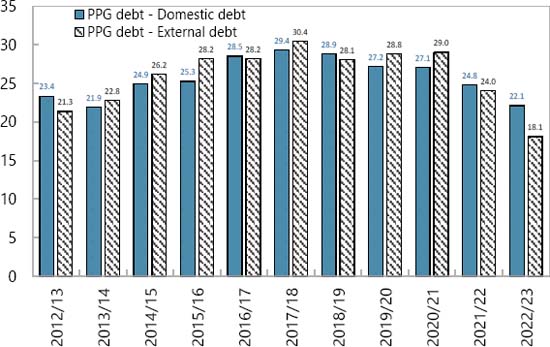

The government has reported improvements in its debt profile. Planning and Development Minister Fitsum Assefa (PhD) announced that Ethiopia had ceased relying on commercial loans and direct borrowing from the central bank.

She noted a significant drop in the external debt-to-GDP ratio to 13.7 per cent, though

the IMF’s Debt Sustainability Analysis, published in July 2024, pegged the ratio at 18

per cent as of June 2023.

External debt accounts for 45 per cent of Ethiopia’s total public and publicly guaranteed

debt, the report stated.

Financing Challenges Persist

Despite these reforms, Ethiopia’s financing challenges remain acute.

The government is seeking nearly USD 1 billion to complete the Koysha Hydroelectric

Dam project, which has stalled at two-thirds completion due to funding shortfalls.

The project is a critical component of Ethiopia’s development strategy, but its delays

underscore the broader fiscal pressures the country faces.

Expert Views on Economic Outlook

While Ethiopian officials are optimistic about the December review as a turning point,

analysts caution that real progress hinges on creditor consensus and the government’s

ability to implement reforms.

Critics have also raised concerns about inflated GDP growth figures, which they argue

may distort Ethiopia’s true debt sustainability.

Looking Ahead

The IMF review, coupled with Ethiopia’s active engagement with creditors, could mark a

a significant step forward in its quest for debt relief.

December will likely be a defining month for the country’s economic future, with broader

implications for its ability to attract investment and complete critical infrastructure

projects.

: KCB Group reports Sh44.5B ( US$ 342.31) nine-month profit, outpacing

Equity Bank. Learn about its 49% growth, challenges, and stock performance this

year.

KCB Group Plc has outperformed Equity Bank to cement its position as Kenya’s leading

lender, posting a net profit of Sh44.5 billion for the nine months ending September

This represents a 49% year-on-year growth, surpassing Equity Bank’s Sh37.5

billion profit during the same period.

Profit Growth Driven by Core Business Performance

The remarkable profit growth was fueled by higher earnings from both interest and non-

interest income streams. KCB’s diverse revenue base has been pivotal in maintaining

its dominance in the competitive banking sector.

Non-Performing Loans a Key Concern

Despite the impressive profit growth, KCB’s non-performing loan (NPL) ratio rose to

18.5%, compared to 16.5% last year. This increase highlights persistent challenges in

managing credit risk, with Chief Financial Officer Lawrence Kimathi acknowledging it as

a “pain point” for the bank.

KCB Stock Outshines Peers on NSE

KCB’s strong financial performance has translated into exceptional stock market results.

The bank’s stock has risen 78.8% year-to-date, making it the best-performing banking

stock on the Nairobi Securities Exchange (NSE).

Plans to Sell National Bank of Kenya

Earlier this year, KCB announced plans to sell its struggling subsidiary, National Bank of

Kenya (NBK), to Nigeria’s Access Bank. While Nigerian regulators have approved the

deal, it is still awaiting clearance from Kenya’s Central Bank. The sale aims to

streamline KCB’s operations and address losses at NBK.

CEO Paul Russo Optimistic About Year-End Performance

“The journey has not been without its hurdles, but our ability to walk alongside our

customers has driven our success,” said KCB CEO Paul Russo. He expressed

confidence in closing the year on a high note, leveraging improving economic conditions

across the region.

Key Figures at a Glance

● Net Profit: Sh44.5 billion (+49%)

● Non-Performing Loan Ratio: 18.5% (up from 16.5%)

● Stock Performance: +78.8% year-to-date

KCB’s strong performance underscores its resilience in navigating challenges and its

commitment to sustaining growth in Kenya’s banking sector.

Bien Aime Baraza: Kenya’s Top Spotify Artist of 2024

Francis Gaitho: Social Media Influence and Legal Battles

Equity CEO James Mwangi Joins World Bank Jobs Advisory Council

-

Business & Money9 months ago

Business & Money9 months agoEquity Group Announces Kshs 15.1 Billion Dividend Amid Strong Performance

-

Politics3 months ago

Politics3 months agoFred Okengo Matiang’i vs. President William Ruto: A 2027 Election Showdown

-

Politics2 months ago

Politics2 months agoIchung’wah Faces Mt. Kenya Backlash Over Gachagua Impeachment Support

-

Politics5 months ago

Politics5 months agoPresident Ruto’s Bold Cabinet Dismissal Sparks Hope for Change

-

Politics5 months ago

Politics5 months agoKenya Grapples with Investor Confidence Crisis Amid Tax Protest Fallout

-

Politics5 months ago

Politics5 months agoPresident Ruto’s Lavish Spending Amid Kenya’s Economic Struggles Sparks Outrage

-

Politics4 months ago

Politics4 months agoJohn Mbadi Takes Over Kenya’s Treasury: Challenges Ahead

-

Business & Money1 month ago

Business & Money1 month agoMeet Kariuki Ngari: Standard Chartered Bank’s new CEO of Africa. What’s Next?