Leadership

Upskilling and Continuous Learning: The Keys to Sustainable Leadership

Those in leadership positions should view continuous learning as a magnetic north. In my leadership journey, one key lesson has been that interest and commitment to continuous learning and development, helps one adopt a mindset and behaviour that produces better leadership outcomes, says Peter Ndegwa.

:“ Certainly, leading is not for the faint hearted, but the good news is, leaders can be made through retooling, that is, a continuous culture of investing in your leadership capacity; self-improvement and upskilling, says Peter Waititu Ndegwa.

By Peter Ndegwa,

CEO, Safaricom Plc

A few weeks ago, I was a keynote speaker at the launch of a leadership development programme committed to inspiring and catalysing Africa’s leaders. The programme seeks to increase the number of high-impact managers in the continent.

At the event, Dr. David Oginde, who is the lead for the programme, stated that Africa’s ability to harness its potential “lies in the hands of high impact leaders.” He developed the programme after realising that even though leaders have the desire to provide good leadership, they do not always have the right tools and capabilities to do so.

His sentiments inspired me to reflect on the attributes of good leadership and why upskilling and continuous learning is key for a holistic approach to leadership.

Continuous learning is vital for leaders and organisations to stay ahead. This, more than ever, places more demand on leaders to take on a new role, which they might initially find unfamiliar, that of facilitating continuous learning within their organisations.

Indeed, as I have learnt it’s one thing to want to hold a leadership role, and it’s another to want to do the demanding work that ‘learning to lead’ entails.

Certainly, leading is not for the faint hearted, but the good news is, leaders can be made through retooling, that is, a continuous culture of investing in your leadership capacity; self-improvement and upskilling.

When I started my career at an audit firm, my goal was self-improvement. This helped me transition from accounting to consulting and corporate finance. I would then move to Diageo, specifically to East African Breweries, to head strategy. The following year, I was asked to lead the sales team as the sales director. I would later make another move to become the CFO and from there I later transitioned into the MD/CEO role.

The transition to different roles enabled me to upskill and fill the gaps in my various leadership roles. My experience and encounters have also taught me that good leadership requires a strong and intentional yearning for self-improvement. It is also important to keep evolving because you don’t have to know everything; you just need to be ready to learn and be guided on new approaches.

I am intentional about building the leadership skills, attributes and capacity. Experience has taught me occupying a leadership position is not the same as leading. To lead, you must be able to connect, motivate, and inspire a sense of ownership of shared objectives.

Therefore, sustainable leadership requires a continuous pursuit of personal development. Perhaps the late John F. Kennedy put it best when he said, “Leadership and learning are indispensable to each other.”

Leaders who are receptive to learning make themselves smaller than the moment. They know they can’t fix everything alone, so they create the space for others to join them and find solutions together.

Those in leadership positions should view continuous learning as a magnetic north. In my leadership journey, one key lesson has been that, interest and commitment to continuous learning and development, helps one adopt a mindset and behaviour that produces better leadership outcomes.

And those outcomes can never be better demonstrated than when leading through disruptive times. One of the things I have come to appreciate in my leadership journey, is the need to be authentic and being conscious of the fact that you are vulnerable rather than hiding your fears in the face of a crisis.

At any one given time every leader is dealing with a crisis. And when several crises converge at once the challenge is even greater. It could be internal or external, and involve various stakeholders such as employees, customers, partners or even an ever-changing business environment.

In such times, the feeling of vulnerability triggers a leader into taking the best course of action for the organization and, at the same time, have the wisdom to understand when to refine their course of action. This involves being able to make decisions faster and leading change efficiently, while skillfully influencing in a more interconnected, collaborative approach with all stakeholders

Admittedly, the leadership journey is a gradual race, one that goes through valleys, smaller peaks before you get to the ultimate peak. The journey of self-improvement in leadership is fascinating and fulfilling if you embrace it.

Especially as you navigate disruptive times but staying the course for a sustainable and progressive future.

First published in the Sunday Nation on 8th February 2022

Leadership

Dr Peter Ndegwa Leads East Africa’s Top Company by Market Value

Dr. Peter Ndegwa leads Safaricom’s enterprise expansion, driving innovation in cloud services, cybersecurity, and IoT to empower sectors like healthcare and education, shaping Kenya’s digital economy.

: Discover how Safaricom, East Africa’s top company by market cap at $5.5 billion, continues to lead the region’s telecom sector under visionary CEO Dr. Peter Ndegwa.

Since taking the helm at Safaricom PLC in April 2020, Dr Peter Ndegwa has steered the telecommunications giant into a new era of growth and transformation.

Safaricom, best known for M-PESA, its groundbreaking mobile payment platform, has continued to evolve under Ndegwa’s leadership, further cementing its position as a key player in Africa’s digital economy.

Known for his strategic focus and innovative mindset, Ndegwa has achieved a series of significant milestones that reflect both his dedication to Safaricom’s mission and his responsiveness to the demands of a fast-changing industry.

In 2024, Safaricom made headlines by reducing Ndegwa’s annual bonus by KSh62 million.

This decision, though surprising, aligns with the company’s broader strategy of reinvesting in expansion, especially in Ethiopia.

Safaricom’s entry into Ethiopia, one of Africa’s most untapped telecom markets, is a major achievement under Dr. Ndegwa’s leadership, requiring substantial capital and adept navigation of regulatory hurdles.

By 2024, Safaricom Ethiopia had attracted 4.6 million subscribers, a feat that not only signals the potential of this market but also demonstrates the resilience and agility that Ndegwa has instilled within Safaricom.

The bold decision to channel resources into this high-stakes venture underscores the company’s commitment to long-term growth over immediate executive rewards, signalling a strategic shift towards sustainable development.

Central to Dr Ndegwa’s vision has been the continued evolution of M-PESA, which he expanded into a comprehensive financial ecosystem through integrations with global platforms and the introduction of the M-PESA Super App.

This app, with a variety of mini-apps catering to different services, has strengthened M-PESA’s position as a pillar of financial inclusion across East Africa.

Safaricom’s commitment to enhancing digital financial services has driven up transaction volumes and revenue, making M-PESA a vital part of Kenya’s economic framework and a model for other markets looking to bridge financial access gaps.

Ndegwa has also championed digital transformation through products that respond directly to customer needs.

The Safaricom MyCounty app, launched in partnership with county governments, is one of these innovations. By offering essential services through mobile, the app represents Dr Ndegwa’s commitment to customer-centric innovation, further reinforcing Safaricom as a digital solutions leader.

Beyond consumer services, Dr Ndegwa has prioritised the expansion of Safaricom’s enterprise segment, offering technology solutions such as cloud services, cybersecurity, and IoT to various sectors including healthcare and education.

This growth in enterprise offerings reflects Safaricom’s role as an enabler of Kenya’s digital economy, diversifying revenue streams while positioning itself as a trusted partner for businesses.

On the technology front, Ndegwa oversaw the rollout of Kenya’s first 5G network in 2021, expanding its reach to multiple cities.

This advancement not only offers faster, more reliable internet but also lays the foundation for future innovations across sectors, reinforcing Safaricom’s competitive edge in data services.

Social responsibility is a key component of Dr Ndegwa’s approach. Safaricom, under his leadership, has committed to becoming a net-zero carbon emitter by 2050, setting a new standard for corporate sustainability in Kenya.

Safaricom’s programs in education, healthcare, and economic empowerment have further cemented its brand as a socially responsible organisation that contributes meaningfully to society.

Despite challenging economic conditions, Dr Ndegwa has maintained Safaricom’s strong financial performance by focusing on operational efficiency and product innovation.

His resilience and adaptability have enabled Safaricom to thrive amid inflation and currency fluctuations, with M-PESA and data services driving revenue growth.

In recognition of his accomplishments, Ndegwa received an Honourary Doctorate in Business Management from Meru University in October 2024, where he also serves as Chancellor.

This accolade reflects his contributions not only to Safaricom but also to Kenya’s business landscape, underscoring his commitment to inspiring future leaders.

Dr.Ndegwa’s appointment as Safaricom’s first Kenyan CEO was a pivotal moment, as previous CEOs were expatriates.

Following the passing of his predecessor Bob Collymore, both the board and the government showed strong support for appointing a local leader.

Michael Joseph, Safaricom’s former CEO and interim head during the transition, highlighted the desire for a Kenyan to lead the company, a sentiment echoed by former

By aligning executive rewards with Safaricom’s evolving performance goals and reinvesting resources into expansion, Ndegwa demonstrates a long-term commitment to growth.

His journey as CEO showcases how he has successfully balanced local roots with a global outlook, driving Safaricom’s mission to transform lives across Kenya and beyond.

Leadership

Financial Institutions’ Crucial Role in Driving Climate Action Beyond COP29

As climate change intensifies and temperatures rise, substantial investments in sustainable practices and technologies are essential. Financial institutions play a crucial role in unlocking the funding needed for transformative change, making their engagement vital to achieving the ambitious targets set at COP conventions.

: At COP 29, financial institutions are key to unlocking funds for climate action, advancing sustainable practices, and supporting global efforts for a greener future.

By Paul Russo, Kenya Commercial Bank CEO

As the UN Climate Change Conference (COP 29) in Baku, Azerbaijan, gets underway today ( November 11), the spotlight is on the pivotal role financial institutions will play in addressing the escalating climate crisis.

Delegates will be seeking global collaboration on tackling the climate crisis with urgency and ambition, as a follow-up to the commitments made in the previous years.

This year’s 10-day conference is poised to build on the momentum established at COP 28, where countries and stakeholders came together to reaffirm their commitment to climate action amidst the urgent need for robust financial mechanisms.

The discussions in Dubai last year emphasised the need for scaled-up funding for climate adaptation and mitigation, with a particular focus on the role of public and private financial flows in achieving net zero transitions.

One of the key outcomes was the reaffirmation of the pledge to mobilise $100 billion annually from developed countries to support developing nations in their climate efforts.

This commitment has laid a foundation for COP 29 discussions on innovative financing solutions and the need for inclusive financing.

Additionally, the establishment of the Loss and Damage Fund highlighted the urgency for financial entities to address the disproportionate impacts of climate change on vulnerable populations, further underscoring the necessity of a robust financial response in the face of global warming. models that ensure equitable access to climate finance.

With climate change intensifying and global temperatures rising, the need for substantial investments in sustainable practices and technologies is paramount.

Financial institutions hold the keys to unlocking funding necessary for transformative change, and their engagement is essential to meeting the ambitious targets that will be set during the COP conventions.

The United Nations Environment Programme estimates that about $4 trillion annually must be mobilised by 2030 to limit global warming to 1.5 degrees Celsius.

This figure is staggering, underscoring the magnitude of the challenge we face and the urgent need for financial institutions to step up.

Financial institutions are uniquely positioned to facilitate this transition. They can provide the necessary capital for renewable energy projects, sustainable infrastructure and green technologies which are integral to reducing greenhouse gas emissions and fostering the green transition.

A report from the International Finance Corporation indicates that investments in renewable energy could create over 24 million jobs globally by 2030, a statistic that could resonate with both policymakers and investors.

The Central Bank of Kenya has introduced initiatives aimed at promoting sustainable banking practices, including the Kenya Green Finance Taxonomy, aimed at classifying environmentally sustainable economic activities.

The taxonomy is aligned with international green finance standards, such as those set by the Climate Bonds Initiative and the European Union Taxonomy for Sustainable Activities.

This helps position Kenya’s green finance sector within the global market, making it easier for investors to participate in Kenya’s green economy.

Financial institutions in Kenya are increasingly adopting Environmental, Social, and Governance (ESG) criteria in their business strategies.

A recent report from the Nairobi Securities Exchange indicated that companies with robust ESG frameworks experience better financial performance and lower risk levels.

It is therefore imperious for financial institutions to recognise their pivotal role in the fight against climate change.

They must embrace the challenge of mobilising the necessary funds while seamlessly integrating sustainability into their operations. The stakes are high, and the time for action is now.

There is a pressing need for the development of innovative green financial products that cater to a wide range of investors and sectors.

To address this challenge, financial institutions must collaborate with various stakeholders to create comprehensive strategies that align financial resources with the urgent needs of climate adaptation and mitigation.

Moreover, these institutions bear the responsibility of integrating climate risk assessments into their decision-making processes, ensuring their portfolios are resilient against the impacts of climate change.

Considering the COP 29 theme, “In Solidarity for a Greener World,” it is crucial for financial institutions to unify their commitment to sustainable practices and collaborative efforts for a healthier planet. Together, we can create a resilient future that prioritises both environmental integrity and economic prosperity.

Leadership

Embracing a new era of globalisation: Balancing growth with sustainability

Kenya is embracing technology and digital tools across key economic sectors, particularly finance. Eighty-seven percent of Kenyan business leaders believe decentralized finance, powered by technologies like blockchain, will foster a more equitable financial system. This can be achieved through international technological collaboration, enhancing digital assets and yielding positive outcomes.

:Exploring the resilience of Kenya’s private sector amidst global challenges

By Kariuki Ngari, Managing Director and Chief Executive Officer, Standard Chartered Kenya and Africa.

In an era characterised by unprecedented global challenges, from supply chain disruptions to geopolitical tensions, the resilience and adaptability of our private sector remain more critical than ever.

I am reminded of a recent interaction I had with Adhiambo one evening. Adhiambo is a fabric trader who sells customised fabrics online.

Her business has undergone no less than 10 iterations in the last year, as she optimises her products for global customers.

Despite several setbacks related to her business model, she believes in her dream to tap into the global marketplace using digital channels.

Not surprisingly, her optimism is mirrored across Kenya’s private sector.

According to the “Resetting Globalisation: Catalysts for Change” report recently released by Standard Chartered, 81% of Kenyan business leaders agree that global trade allows for sustainable development, where no one is left out of the global economy.

The report captures insights from over 3,000 business leaders worldwide, shedding light on the very resilient and evolving nature of globalisation.

Our research shows that business leaders in Kenya are most confident about the role that capital plays in globalisation and they are amongst the most likely to say that foreign investment has been instrumental to the growth and development of their economy.

Kenyan business leaders are also more likely than their peers in the other 19 markets surveyed to say that the solutions for climate change require a localised approach.

The report reveals a surprising confidence among business leaders in globalisation and trade, despite recent hurdles.

This confidence isn’t blind optimism; it’s grounded in a recognition of the undeniable benefits that global trade has brought, particularly in sustainable development. A staggering 86% of leaders acknowledge this positive impact, challenging the growing scepticism around globalisation.

An essential aspect of this new globalisation is the emphasis on inclusivity and sustainability. There’s a pressing need to balance growth with sustainability, especially in developing markets.

The report’s findings suggest that global trade isn’t just an economic engine; it’s a catalyst for sustainable practices and innovation.

This perspective is crucial as we navigate the complexities of environmental challenges and social inequalities.

49% of Kenyan business leaders believe that if sustainability is kept a paramount consideration, then countries should support the movement of goods and services with the least friction possible. There is hope for Adhiambo.

Moreover, the report highlights the importance of free capital flow. Almost all business leaders (95%) agree on this need – and 97% in Kenya, underscoring the role of financial markets in fostering growth in both developed and developing economies. This perspective is pivotal, considering the increasing global focus on equitable economic development.

However, it’s not just about capital and trade. The digital revolution has brought the world closer, with 75% of leaders acknowledging the positive outcomes of the free flow of data. This digital interconnectedness is reshaping how we think about finance, security, and talent mobility. The global talent pool, as highlighted by 74% of leaders, has become a cornerstone for innovative and diverse business practices.

Responsible investments find favour in Africa

Kenya is a country adopting the widespread use of technology and digital tools in crucial economic sectors, including finance. Eighty-seven per cent of Kenyan business leaders say that decentralised finance, which runs on technologies such as blockchain, will create a more equitable financial system.

This can be achieved through the sharing of technological progress between countries, allowing for the strengthening of digital assets and resulting in a positive outcome.

A surprising finding from the report is that business leaders from emerging economies are more likely to trade higher returns for more responsible investments than their counterparts from the developed world.

Those from Kenya (45%), Nigeria (46%) and China (44%) are among the most likely to trade in higher returns for a more sustainable and responsible investment opportunity.

From a global perspective, 59% agree that finding the highest returns is the most crucial factor in their investment decisions. A great example of this is in Switzerland where only one in four investors would select a more responsible investment.

Despite these positive attitudes, the path ahead is not without its challenges. Global governance mechanisms, while effective in some areas, need to be re-evaluated and restructured to address the nuances of today’s global issues, particularly in environmental matters.

The report indicates a mixed response on the effectiveness of these mechanisms, with 70% of leaders viewing them positively.

In conclusion, business leaders must respond to this call to action. We must rethink globalisation, not as a passive concept but as a dynamic, evolving process.

The next chapter of globalisation is not just about economic growth. It is about creating a fairer, more inclusive world, where technological progress benefits all, and sustainability is not just an afterthought but a guiding principle.

In the words of Bill Winters, Group Chief Executive of Standard Chartered, we need a “just transition” to ensure continued economic development without sacrificing our planet or leaving anyone behind.

The future of globalisation is not just in the hands of policymakers and business leaders; it’s in our collective effort to shape a world that values connection, collaboration, and sustainable growth.

Keywords:Resilience:Globalisation:Sustainability:Inclusivity: Digital Transformation

DTB Group Reports 8.4% Profit Rise to Sh6.5B in Nine Months

Kenya & Mauritius Lead East Africa’s Cybercrime Battle

Anthony Kituuka Resigns as Equity Bank Uganda MD Amid SectorWoes.

-

Business & Money8 months ago

Business & Money8 months agoEquity Group Announces Kshs 15.1 Billion Dividend Amid Strong Performance

-

Politics3 months ago

Politics3 months agoFred Okengo Matiang’i vs. President William Ruto: A 2027 Election Showdown

-

Politics2 months ago

Politics2 months agoIchung’wah Faces Mt. Kenya Backlash Over Gachagua Impeachment Support

-

Politics5 months ago

Politics5 months agoPresident Ruto’s Bold Cabinet Dismissal Sparks Hope for Change

-

Politics5 months ago

Politics5 months agoKenya Grapples with Investor Confidence Crisis Amid Tax Protest Fallout

-

Politics5 months ago

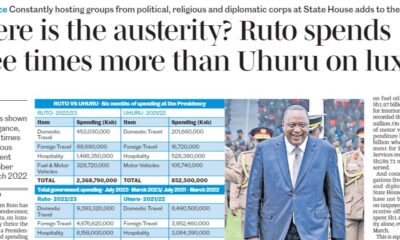

Politics5 months agoPresident Ruto’s Lavish Spending Amid Kenya’s Economic Struggles Sparks Outrage

-

Politics4 months ago

Politics4 months agoJohn Mbadi Takes Over Kenya’s Treasury: Challenges Ahead

-

Business & Money3 weeks ago

Business & Money3 weeks agoMeet Kariuki Ngari: Standard Chartered Bank’s new CEO of Africa. What’s Next?